The year started off on a good note, with markets buoyed by strong corporate earnings expectations, a business-friendly administration, and low interest rates. The war with Iran shifted the market’s focus towards the Middle East and assets began trading off daily news headlines. However, despite the geopolitical tensions, rising oil prices, and higher interest rates, the U.S. economy remained resilient. The stock market showed the same resilience and soon recovered its all-time highs. We stayed invested through the turbulence and were rewarded for looking past the headlines and avoiding emotional decision making.

Strategy Asset Managers’ portfolios were well positioned prior to the war and as such have performed strongly in the year-to-date. Our stock selection and understanding of the market environment allowed us to pre-position into resilient investments with the potential to thrive in the months and years ahead. Oil & gas, aerospace & defense, shipping, and staples stocks performed well in the 1st quarter, largely because of the war. Growth stocks declined as the stock market broadened into dividend paying stocks and out of the “Magnificent Seven,” while foreign stocks suffered from their exposure to energy prices.

Market Behavior

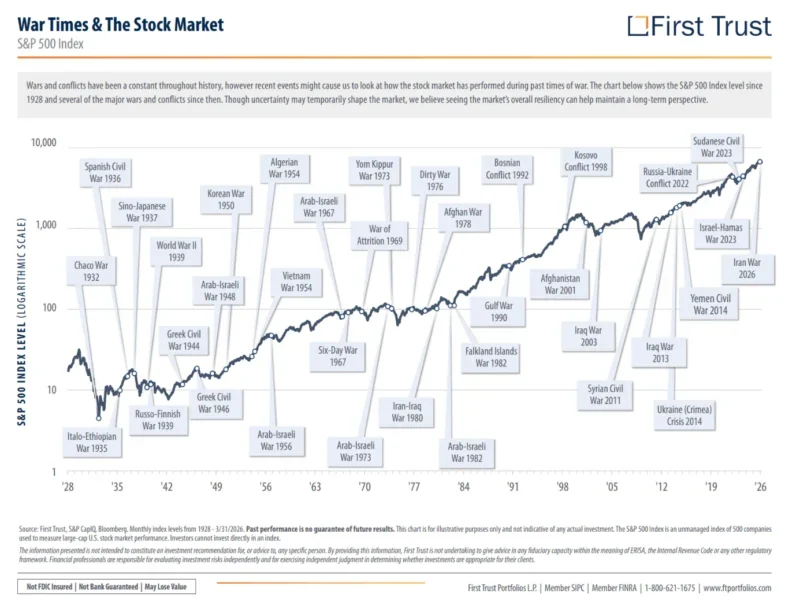

While the short-term path is uncertain, the past 125 years of U.S. history shows that wars and geopolitical shocks do not derail the stock market long-term.

War and the Stock Market

We do not trade off news headlines or emotions and instead focus on the factors that drive stocks over longer periods of time. Markets typically experience a 5%-10% pullback every year, and last year stocks did decline by 20% around April. The 10% decline that we saw in the 1st quarter was very typical, and these corrections occur often during both good and bad economic conditions. This conflict has not yet changed our long-term outlook on the markets.

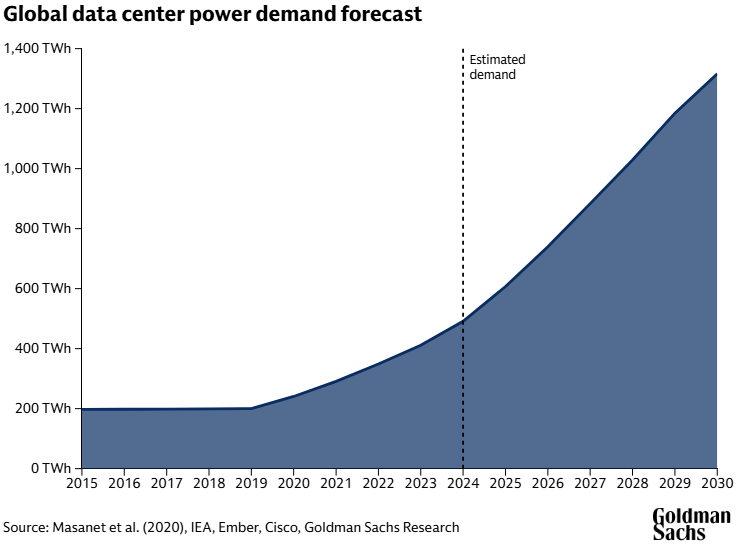

Growing Demand for Power

Electricity is the lifeblood of Artificial Intelligence, and we believe that nuclear energy specifically will play a critical role. A new analysis from Wood Mackenzie shows that 220 gigawatts of additional power demand from data centers is in the pipeline in the U.S. That is a massive amount, equal to about 22% of U.S. peak demand.

Global Data Center Power Demand

Although less important than in the past, energy prices are still nearly 4% of consumer spending, with a significant impact on inflation and therefore monetary policy. Higher gasoline prices act as a tax hike on consumers, depressing spending but while bolstering inflation. Markets no longer expect any interest cuts through mid-2027.

However, strong earnings growth tends to insulate against steep stock market declines. If history is any guide, corrections are possible but generally contained while earnings are growing. Even in deeper corrections, rebounds tend to come relatively quickly. Estimates currently call for 17% S&P 500 earnings growth in both 2026 and 2027.

Available indicators suggest that U.S. economic activity has been expanding at a solid pace. Job gains have remained low, and the unemployment rate has been largely unchanged in recent months.

While the economy presently appears strong, a sustained period of severe oil disruption would eventually weigh on economic growth and therefore earnings. It is estimated that every 1% change in real US GDP growth corresponds to a 3-4% change in S&P 500 earnings. Uncertainty could also undermine corporate confidence and impact planned capital expenditures.

Why the U.S. is Better Positioned

As the largest energy producer in the world, America is one of the country’s best positioned to endure the rapid spike in energy prices. The U.S. is the largest exporter of liquefied natural gas and a major producer of fertilizer, helium, and other natural resources. This strong position has muted the war’s impact, at least thus far.

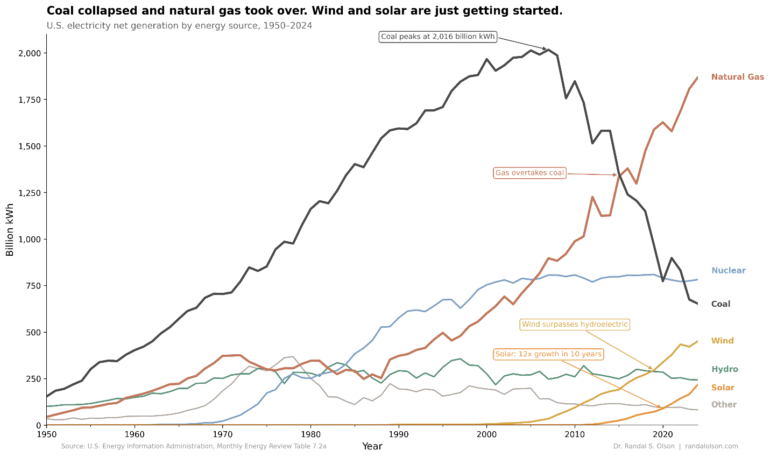

U.S. Electricity Generation by Source

In addition, U.S. consumers spend a significantly smaller portion of their income on food and gasoline than in the past. In 1970, more than 20% of consumer spending was on food and energy – today that number stands near 10%. As a result, there is very little risk of a 1970’s style inflationary spike here in the U.S., although higher energy prices will naturally bias inflation upwards. Europeans, in contrast, spend 11% of their income on energy and are extremely vulnerable to any spike in prices.

Lastly, the windfall profits earned by U.S. energy producers will be reinvested, helping to stimulate the economy and blunt the war’s impact.

Technology Led Disinflationary Boom

The development of A.I. is still in its early stages, and there will be disruption as new applications arise in the coming years. We are encouraged to see the strength within domestic equities broaden outside of mega-cap technology. A market that is less dependent on its largest names is healthier.

There was recently a very exciting advance in the field of humanoid robots – a humanoid robot ran the fastest half marathon in history. While this was inevitable, the speed of development was incredible – last year the robot took 2 hours and 40 minutes to complete the run, this year it took only 50 minutes. Humanoid robots have the potential to be one of the greatest productivity enhancing innovations in history – imagine how productive people will be if they no longer need to cook or clean or do laundry. While productivity booms are extremely beneficial to society in many ways, one of their greatest benefits is that they allow for disinflationary growth.

A.I., humanoid robots, and autonomous vehicles, amongst many other revolutionary innovations could create a multi-decade period of disinflationary growth akin to the 1800’s. During this century steam engines, telegraphs, railroads, and lightbulbs supercharged productivity, allowing the economy to grow at eye-popping rates without inflation.

What You Should Know

The stock market has remained resilient in the face of geopolitical uncertainty, rising oil prices, and higher interest rates. We know the situation is fluid, but we see earnings growth and opportunities ahead. The U.S. economy is stable and corporate earnings are growing, creating a favorable backdrop for your portfolio.

As always, we will make decisions based on research rather than emotion. The environment thus far this year has favored our approach, and in the balance of the year we will continue to stay active, grounded in fundamentals, and positioned to capitalize on dislocations as they emerge.